The memory market is entering uncharted territory, driven by the rise of agentic AI and its relentless appetite for storage capacity. Demand is no longer just about training large models; it’s about continuous, iterative inference cycles where every recalculation multiplies compute costs exponentially. This shift has forced industry analysts to rewrite their projections entirely.

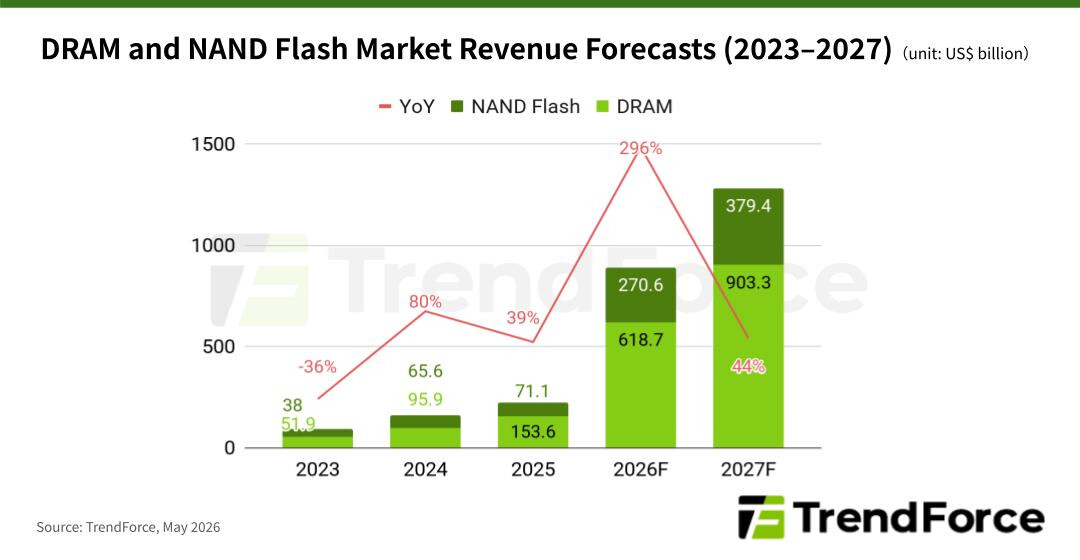

Global memory revenue, already under pressure from AI workloads, is now expected to hit $889.3 billion in 2026—nearly 60% higher than earlier estimates—and could surge past $1.28 trillion by 2027. The growth isn’t just a blip; it represents sustained upward momentum, with annual increases of 44% or more. Behind this surge is a fundamental change in how AI systems operate: inference requests are no longer isolated queries but part of ongoing loops that demand larger KV cache capacities and more efficient memory management.

This isn’t just about DRAM. The shift also impacts NAND flash, where capital expenditures from the largest chip suppliers are rising at 79% annually. High-performance SSD technologies—from SCM to SLC/pSLC—are becoming the backbone of AI infrastructure, filling the gap left by HBM’s high cost and HDDs’ limitations in speed and power efficiency.

Yet for all the talk of growth, the market remains constrained. HBM, despite its advantages, is still too expensive for broad adoption, while traditional DRAM faces wafer shortages that limit supply. The result? Pricing power is shifting decisively toward suppliers, with contract negotiations increasingly favoring upward adjustments well into 2027.

- DRAM Market Forecast:

- 2026: $618.7 billion (303% annual growth)

- 2027: $903.3 billion (46% YoY increase)

The implications for power users are clear. Efficient memory management is no longer optional—it’s a necessity to keep costs in check as demand outpaces supply. For AI servers, the CPU-to-GPU ratio is already evolving from traditional 1:8 configurations toward 1:4 or even 1:2, as seen in NVIDIA’s NVL72 rack. This means more server DRAM capacity is required, but with procurement volumes and pricing still under pressure.

What’s next? The memory crunch isn’t going away anytime soon. With agentic AI continuing to reshape workloads, the market will remain tight, and prices will likely stay elevated. For power users, the key will be balancing performance needs against operational costs—something that will define the next phase of AI infrastructure development.