Memory prices are entering uncharted territory in early 2026, with analysts forecasting the steepest quarterly increases on record across DRAM and NAND Flash. The surge stems from relentless AI-driven demand outpacing production capacity, forcing suppliers to prioritize high-margin contracts while end users—from data centers to smartphones—compete fiercely for limited allocations.

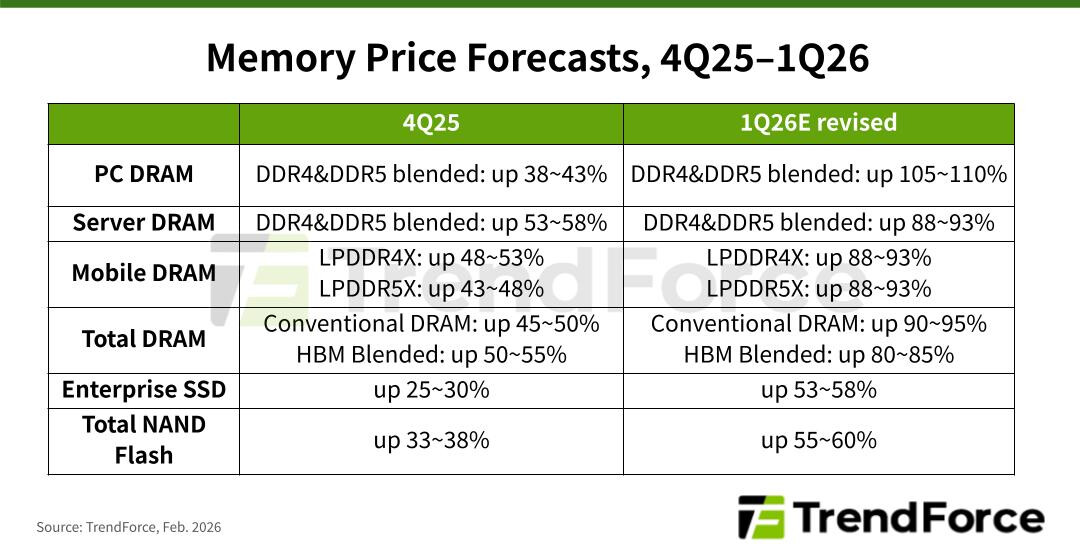

TrendForce’s latest outlook revises upward its projections for conventional DRAM, now expecting contract prices to climb by 90–95% quarter-over-quarter in the first three months of the year, up from earlier estimates of 55–60%. NAND Flash prices, meanwhile, are now anticipated to jump 55–60%, a sharp revision from the 33–38% increase previously forecasted.

At the heart of the crisis is a fundamental imbalance between supply and demand. PC DRAM shortages in late 2025—even among top-tier OEMs—have left inventories dangerously low. With suppliers holding the upper hand, prices for PC-grade DRAM could exceed a 100% increase in 1Q26, marking the largest quarterly spike ever recorded. Server DRAM is not far behind, with North American and Chinese cloud providers locking in long-term agreements that are driving prices up by around 90% as buyers scramble for limited capacity.

The ripple effects extend to mobile memory, where LPDDR4X and LPDDR5X—critical for smartphones and tablets—are also facing near-90% quarterly hikes. Negotiations for U.S.-based brands concluded late last year, but Chinese vendors remain in active discussions, with final contracts expected by late February after accounting for holiday disruptions.

NAND Flash is under similar pressure, despite suppliers redirecting production lines toward DRAM to capitalize on higher profits. Enterprise SSDs, in particular, are seeing demand surge as AI inference workloads expand, with prices projected to rise 53–58%—another record quarterly jump. The bottleneck is exacerbated by incremental process upgrades rather than large-scale capacity expansions, leaving little room for relief in the short term.

Key specs and trends

- DRAM: PC DRAM prices could rise over 100% QoQ; server DRAM up ~90% QoQ.

- Mobile DRAM: LPDDR4X/LPDDR5X contracts up ~90% QoQ.

- NAND Flash: Enterprise SSDs up 53–58% QoQ; suppliers shifting capacity to DRAM.

- Supply shifts: DDR6 production remains limited; DDR4/DDR5 still dominate but face allocation wars.

The implications are far-reaching. For gamers, the cost of high-end GPUs like the RTX 5070 Ti or RTX 5090—already strained by memory shortages—could climb further as DRAM prices feed into system costs. Meanwhile, AI-driven enterprises may face delays or higher costs for storage upgrades, while smartphone manufacturers could pass along price increases to consumers.

With no immediate relief in sight, the first quarter of 2026 is shaping up to be a pivotal moment for the memory market—one that could redefine pricing benchmarks for years to come.