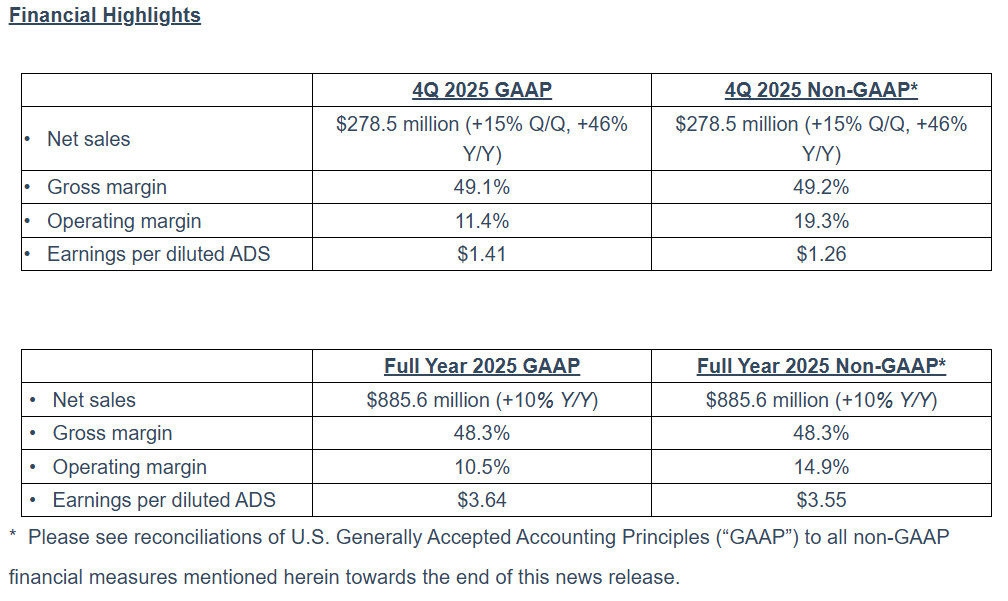

Silicon Motion Technology Corporation closed 2025 with its best quarter yet, posting a 15% increase in net sales to $278.5 million in Q4—outpacing the $242.0 million recorded in Q3. The gains reflect a multi-pronged strategy: aggressive expansion in consumer SSDs, a push into PCIe 5 controllers, and early inroads into enterprise storage, including a notable first sale to a leading GPU maker.

The company’s net income (GAAP) also rose to $47.7 million, up from $39.1 million in Q3, while non-GAAP earnings climbed to $42.7 million from $33.8 million. Per-share earnings followed the same upward trend, with GAAP figures reaching $1.41 per diluted ADS and non-GAAP at $1.26—both higher than the prior quarter’s $1.16 and $1.00, respectively.

A Shift Toward High-Performance Storage

Wallace Kou, President and CEO, highlighted two key drivers behind the growth: the ramp-up of PCIe 5 SSD controllers and sustained gains in eMMC/UFS storage. Client SSD controller sales surged over 25% quarter-over-quarter, with Silicon Motion’s newly introduced 4-channel PCIe 5 controllers gaining traction alongside its established 8-channel models. The automotive segment also saw strong performance, fueled by diversified product offerings and new customer partnerships.

Beyond traditional storage, Silicon Motion made its first enterprise storage sales to a major GPU manufacturer—a move that aligns with broader industry trends toward high-performance boot drives in data centers and AI workloads. While details remain limited, the partnership suggests the company is positioning itself as a supplier for next-gen compute platforms.

Market Share and Long-Term Bets

Silicon Motion’s eMMC and UFS products continued to gain market share in Q4, reinforcing its dominance in embedded storage. The company’s capital expenditures totaled $7.8 million, with $6.2 million allocated to testing equipment, software, and design tools—a sign of ongoing R&D investments in next-generation storage solutions.

Looking ahead, Kou emphasized sustained growth across all business lines, with expectations for continued revenue acceleration in 2026. The company’s backlog for Q1 2026 suggests a stronger-than-seasonal start, though exact figures were not disclosed. Shareholders also benefited from a $2.00 annual dividend, with the first $0.50 installment totaling $16.7 million paid out in November 2025.

The financial results underscore Silicon Motion’s ability to capitalize on shifting storage demands, particularly in PCIe 5 and enterprise applications. However, the company’s reliance on a single high-profile enterprise client remains a wildcard—early traction does not guarantee long-term adoption in a competitive market.